Asset Liability Immunization Strategy (ALIS) Insights 1st Quarter 2025 Outlook

Executive Summary:

- The fourth quarter of 2024 produced rising bond yields due to the Fed’s easing cycle over inflation and deficits, resulting in negative bond returns while the domestic equity market saw positive returns, despite significant dispersion amongst the various sectors.

- Consumer sentiment recently declined, a signal that could translate into reduced spending and lower economic growth while the service sector weakened and inflation measures moved closer to targeted levels, leading to the expectation of only two rate cuts in 2025.

- Past central bank missteps and high equity market valuations suggest caution, with the potential for significant market adjustments if economic conditions deviate too far from expectations.

State of the Markets

During the final quarter of 2024, bond yields rose predicated by the Fed’s easing cycle that began in September, producing negative total returns for bond holdings. This increase is partly due to slow progress in reducing inflation to the Fed’s 2% target and concerns over deficits linked to President Trump’s policies. Tariffs, deportations, onshoring manufacturing, and additional tax cuts have contributed to the yield volatility. If policy missteps negatively impact market participants and voters, rates may reverse. The market's movement suggests a belief in persistent inflationary pressures and federal deficits, although the new administration's actions will ultimately determine the final outcome.

During the quarter, the US domestic equity market experienced positive returns. The broad stock market, as measured by the Russell 3000 Index, rose by 2.6%. Large-cap growth stocks led the way, with the Russell 1000 Growth Index posting a notable 7.1% gain. However, value stocks underperformed, with the Russell 1000 Value Index returning -2%. Small-cap stocks, tracked by the Russell 2000 Index, produced a modest positive return of 0.3%. Dispersion across sectors was significant. Consumer discretionary, financials and communication services were positively influenced by the Mag-7 and expectations for deregulation, while the assumed safety of fixed income securities caused higher yielding sectors to decline as a substitute. International developed and emerging market equities contributed negatively to the overall equity asset class, with returns of -8.1% and -3.1% respectively.

Consumer sentiment recently provided a negative surprise, which may correlate with lower spending and eventually affect economic growth. Meanwhile, the manufacturing sector continues to contract, while the service sector is starting to show signs of weakness. The unemployment rate has fluctuated between 4.0% and 4.2%, essentially indicating full employment. Headline CPI is growing by 2.9%, core CPI is up by 3.3%, and core PCE has increased by 2.8%. Year-over-year, average hourly earnings are 4.1% higher, meaning workers' wages are outpacing inflation. Many inflation measures are beginning to approach more comfortable levels, although the recent ISM Non-Manufacturing Prices subcomponent jumped from 58.2 in November to 64.4 in December, then declined to 60.4 in January. December marked the highest reading since 2023 and the 91st consecutive month of price increases in the service sector. This significant inflationary shock in the crucial services sector has pushed market expectations for the Fed’s next rate cut to July. The Fed’s most recent Dot Plot indicates a likelihood of only two rate cuts in 2025, with the market suggesting cuts totaling slightly more than 50 basis points (bps) for the year.

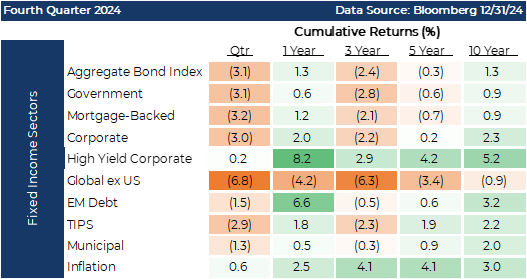

Over the course of the 4th quarter, 10-year Treasury yields increased from 3.78% to 4.57% resulting in negative performance for many sectors, eliminating much of their gains for the year. From the start of the year, 10-year Treasury yields increased by 119 bps. Taxable bond indices experienced year-to-date total returns of between +1.2% to 2.5%. The strongest returns for bonds this past year have been in the shortest-term indices and the lower quality segment. Over the course of the year, corporate bonds outperformed the aggregate bond index, fueled by tighter credit spreads and higher income production. With the degree of uncertainty in the market and the likelihood of a slower pace of Fed rate cuts in 2025, the shorter maturities are shaping up as an area that warrants further allocation in fixed-income portfolios.

Pension Market Update

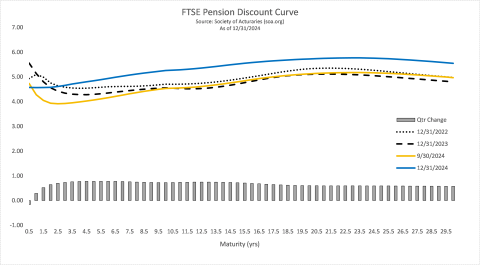

Market movements over the last quarter of 2024 created a dynamic where all seven of the pension indices that we follow exhibited a modest improvement in their level of funding. On average over the quarter, they improved by +2.7% with a year-to-date improvement measuring +7.5%. The average pension index as measured at year-end was funded at just over 108%. Rising discount rates combined with positive risk asset market performance created the perfect storm for pension plan funding improvement and 2024 was not an exception. The FTSE Discount Curve provides a good example of how discount rates behaved over the quarter and year.

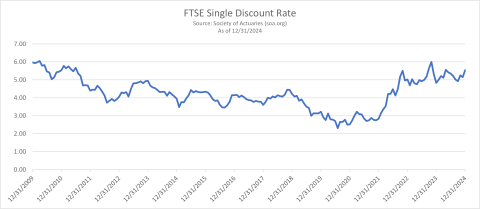

The curve not only showed an improvement over the final quarter (QTD) with an average movement of +39 basis points but also a year-to-date (YTD) improvement on average of +36 bps. The FTSE single rate exhibited the same progression with a QTD upward shift of +62 bps and YTD progress of +71 bps.

Economic Outlook

The Federal Reserve's ability to achieve a soft landing, or perhaps no landing, from the post-pandemic growth period is currently under scrutiny. Inflation has eased, risk asset prices are up, corporate earnings are growing, and job opportunities are plentiful. However, the market seems to have forgotten the Fed's previous misstep with transitory inflation, which led to significant pain for many individuals and families. The Fed's December rate cut was questionable, as progress toward healthy inflation had stalled, and inflationary signs in the service sector have since increased. Keep in mind that expectations often drive inflation measures. The December rate cut may have been a cover for continued Quantitative Tightening, reducing their balance sheet to give themselves the ability to face the next market event.

Despite recent declines in the stock market and lower bond yields, investor optimism has remained resilient. Early in Q4, stock market optimism saw its biggest jump since June 2020. Warren Buffet's measure of stock market capitalization as a percentage of GDP suggests valuations are high, with the current level at 133%. Buffet's recent stock sales indicate he believes stock valuations are outsized, favoring cash equivalents for better risk-adjusted returns. Since the S&P 500 recent low point in 2022, stocks are up roughly 70%. Examples of investor enthusiasm include Broadcom trading at 21 times revenue compared to Proctor & Gamble's five times, and MicroStrategy's stock trading at 150% of its Bitcoin value. The bond market also reflects positivity, with risk spreads for investment-grade bonds at their lowest since 1998. High yield bonds have seen similar spread tightening. However, a wave of credit upgrades since the pandemic has improved the perceived quality of corporate bonds. Higher market coupons have reduced interest rate risk, but the likelihood of spread widening remains if the economy slows. Last quarter, we predicted 10-year Treasuries would retest the 4.50% area and drop below 3% during the weakest part of 2025. If 10-year Treasuries exceed 5%, they may test levels closer to 5.5%, with a floor forecast of 3%. Fiscal discipline or events triggering a flight to quality could lead to decent bond returns in 2025. Historically, higher purchased (book) yields correlate with better forward-looking total returns, which is a message that is particularly important for our pension clients. Both stock and bond markets have perfection priced in, and any deviation from this could lead to price adjustments or stagnation. The U.S. market differs from Japan's, but the Nikkei 225 Index took 34 years to recover after its peak in 1989. Exuberance can lead to hardship, and caution is advised in this market environment.

Credit levels and delinquency trends remain concerning. Despite wage growth keeping pace with inflation, high debt levels at over 20% interest rates will strain family budgets. The end of the student loan repayment holiday will also add further pressures. Home affordability remains an issue with 30-year mortgage rates near 7%. Many consumers are burdened by various forms of high-interest credit, leading to potential future consumption shocks. Economic risks include shrinking money supply, political uncertainty, and demographic challenges. Commercial real estate (CRE) faces significant losses, and private credit markets offer little illiquidity premium. We monitor early signs of economic weakening, such as the declining number of temporary workers, which often precedes recessions. Despite small business optimism post-election, the reduction in temporary workers and return to in-office work weeks suggest companies are preparing for leaner operations.

Embracing the uncertainty of the future can be liberating. The next two years may require discerning key developments from market noise. President-Elect Trump's cabinet picks seem serious and not political minions, which is positive. The challenge is whether meaningful deficit reduction can occur alongside economic growth. Potential economic paths include growth and tariff policies that could stoke inflation, driving bond yields higher. Alternatively, if Trump's policies fail, a fiscal spending "Hail Mary" might be needed. We expect a push-and-pull economy with waves of positivity and shocks. Elon Musk's non-traditional approach to government efficiency will be interesting to watch. Consumers may eventually struggle with too many obligations and insufficient assets or cash flow, as productivity gains and wage improvements seem unlikely in the near term.

Historically, higher purchased yields in bond portfolios lead to favor positive total returns. High borrowing costs and record debt levels for consumers and the U.S. government demand a change in trajectory. The Fed is likely on hold until the latter half of 2025, making short-term bonds a stable part of our previously advised barbell strategy. They also offer attractive yields with minimal interest rate risk. As consumers show signs of exhaustion, the economy may slow, benefiting from the longer segment of a barbell approach.

Investment advisory services are offered through Advanced Capital Group (“ACG”), an SEC registered investment adviser. The information provided herein is intended to be informative in nature and not intended to be advice relative to any specific investment or portfolio offered through ACG. The views expressed in this commentary reflect the opinion of the presenter based on data available as of the date this was written and is subject to change without notice. Information used is from sources deemed to be reliable. ACG is not liable for errors from these third sources. This commentary is not a complete analysis of any sector, industry, or security. The information provided in this commentary is not a solicitation for the investment management services of ACG and is for educational purposes only. References to specific securities are solely for illustration and education, relative to the market and related commentary. Individual investors should consult with their financial advisor before implementing changes in their portfolio based on opinions expressed.